Short-term disability coverage is a great way to protect your income when you are unable to work due to temporary conditions like illness, injury, or maternity leave.

These benefits can replace part of your income during a short time span. Employers often provide this insurance as part of a compensation package, but you may also purchase it on your own.

If you receive short-term disability benefits, you may be wondering if the benefits are taxable. You are not alone in this concern. Many people are unsure of what to expect when it comes to taxes and disability benefits.

Is Short-Term Disability Taxable? Generally, the short-term disability payments are taxable if your employer paid the premiums in full or in part. Also, it is taxable if you paid your own premiums (or a portion of them) with pretax dollars. However, if you paid your own short-term disability plan with after-tax dollars, then the payments you receive from the plan are not considered taxable income.

Consult with your tax advisor to find out whether your short-term disability payments are taxable.

In this post, we’ll break down everything you need to know about short-term disability benefits and taxation. In addition, we will explain how these benefits are taxed.

So, if you’re unsure whether or not your short-term disability benefits are taxable, keep reading!

Is Short-Term Disability Taxable?

The answer to the question will vary depending on the condition. Short-term disability benefit is generally taxable, however, there are some exceptions.

Short-term disability is a type of insurance that replaces a portion of your income if you are unable to work for a short period of time due to an illness or injury.

Usually, it pays anywhere from 40% to 70% of your salary. The benefits typically last from three to six months. However, some plans may cover the disability for one or even two years.

To determine whether short-term disability benefits are taxable, you must look at who and how paid the premiums.

Here’s how it works:

- All of your short-term disability income is taxable if your employer paid 100% of your premiums.

- Your half of the premiums would be taxed if you split it 50/50 with your employer and you paid your portion of the premiums with after-tax dollars (rather than paycheck deductions).

- Your short-term disability benefits are not taxable if you paid all your premiums yourself with after-tax dollars.

If you are not sure whether your particular situation falls into one of these categories, it is best to speak with a tax professional. They can help determine if your benefits are taxable.

Calculating Tax On Short-Term Disability Benefits

If your short-term disability (STD) benefits are considered taxable income, you will need to calculate the taxes on these benefits. You can do this by using a tax calculator or by speaking to a tax professional.

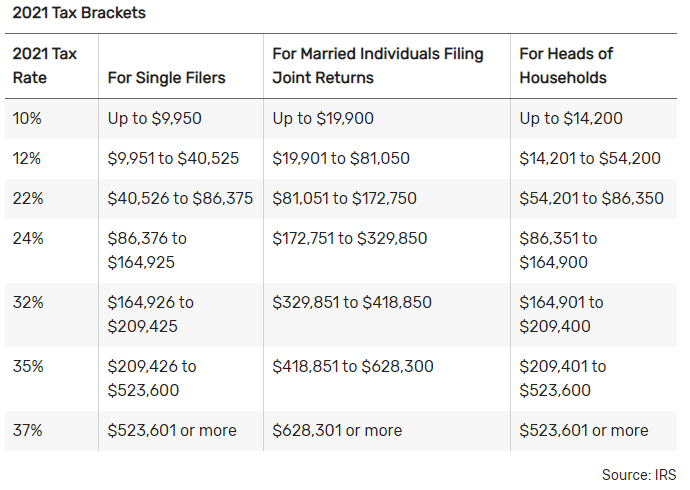

When calculating the STD taxes, you will need to take into account the marginal tax rate. The marginal tax rate is the rate at which the last dollar you earn is taxed. There are seven marginal tax brackets or rates in 2022: 10%, 12%, 22%, 24%, 32%, 35%, and 37%.

Below is a breakdown of tax brackets, by filing status, for the tax years 2021 and 2022.

Tax Tables For The Tax Year 2021 (Filed In 2022)

From January 1 through December 31, 2021, these tax rates are in effect.

Tax Tables For The Tax Year 2022 (Filed In 2023)

These tax rates will apply to income earned from January 1 through December 31, 2022.

To calculate tax on Short-Term Disability, you will need to know your income and your taxable disability benefits. Your taxable disability benefits are part of your short-term disability payments that are considered taxable income.

To find this amount, subtract any non-taxable portion of your payments from the total amount of your payments. The result is the amount of your taxable disability benefits.

Now that you know the amount of your taxable disability benefits, multiply this number by your marginal tax rate. This is the tax you will owe on your short-term disability payments. For example, if you received $10,000 in short-term disability benefits and your marginal tax rate is 25%, you would owe $2,500 in taxes.

If you have any questions about how to calculate your taxes, you should consult a tax professional.

How To File Short Term Disability Benefits On Your Federal Taxes

If your short-term disability benefits are considered taxable income, you will need to report this income on your federal tax return. You must report this income, including short-term disability benefits, on Form 1040 or 1040-EZ.

For example, let’s assume that in the tax year 2021, you collect $9,000 in short-term disability benefits. Half of your premiums were paid by your employer, and the other half was deducted from your paychecks as pre-tax withholding.

The entire $9,000 is taxable income and you must report it on your Form 1040. You should include this amount in line 1 of your 2021 return, along with all of your wages, salaries, and tips. You can find the taxable amount on the W-2 form you received from your employer.

State Taxes On Short Term Disability Benefits

State taxes on short-term disability benefits vary by state. Some states do not tax short-term disability benefits at all, while others tax them as regular income. It’s crucial to check with your state’s revenue department to find out how your state taxes disability benefits.

However, most states treat short-term disability benefits as taxable income. This means that you will have to pay income tax on the amount of money you receive in disability benefits. In addition, you may also have to pay Social Security and Medicare taxes on those benefits.

If you live in one of the nine states (see below) without an income tax, then taxation only comes from the federal government.

- Alaska

- Florida

- Nevada

- North Dakota (taxes only interest and dividend income)

- South Dakota

- Tennessee

- Texas

- Washington

- Wyoming

Some states, such as New York and Hawaii, partially tax these benefits based on how much your employer pays for the insurance and how much you pay for it.

However, if you live in New Jersey, California, or Rhode Island, short-term disability benefits are not taxed at the state level but may be taxed by the IRS under certain circumstances.

For example, if an employer in New Jersey is required to treat short-term disability benefits as third-party sick pay, then the IRS may tax those benefits at the federal level, even though they are not taxed at the state level. This includes the half of FICA taxes (Social Security and Medicare) that employers have to pay.

Similarly, in California, employees are required to pay into the state’s disability insurance program through payroll deductions, but the IRS only taxes these benefits if they are considered to be a substitute for unemployment insurance. If this is the case, then the employer should send you a Form 1099-G reporting the income. Otherwise, your short-term disability benefits are not taxable.

Consult your employer’s human resources department or a local tax professional if you’re unsure if the short-term disability is taxable in your state.

Conclusion

So, is short-term disability taxable? The answer is, it depends. If your employer pays the premiums for your short-term disability insurance, then the benefits are considered taxable income. However, if you pay the premiums with after-tax dollars, then the benefits are not considered taxable income.

In addition, how your state taxes short-term disability benefits may differ from how the federal government taxes them. Some states, such as New York and Hawaii, partially tax these benefits, while others, such as California and New Jersey, do not tax them.

It is best to check with your state’s revenue department to determine to find out if these benefits are taxed in your state.