Social Security benefits are a form of government assistance that a lot of people rely on. But when it comes to the taxability of Social Security benefits, there are a lot of misconceptions.

Is Social Security Taxable? Yes, Social Security benefits are taxable at the federal level and in certain states as well. The benefits are taxable if your provisional or combined income is above a certain limit (we’ll talk more about that below). Your combined income is your adjusted gross income plus any nontaxable interest you have plus half of your social security benefits.

In this blog post, we’ll explain whether Social Security benefits are taxable and how they are calculated. We’ll also give you some tips on how to minimize the amount of tax you have to pay on your benefits.

For example, many people believe that all of their Social Security income is taxed. However, that’s not always the case.

So, whether you’re just starting to collect Social Security or you’re nearing retirement age, read on for everything you need to know about the taxability of Social Security benefits.

Is Social Security Taxable?

Yes, Social security benefits are usually taxable. Social Security benefits are a federal program that provides monthly payments to eligible retirees, disabled workers, and the surviving spouses and children of deceased workers.

Eligibility for social security benefits is based on the worker’s lifetime earnings history. Workers must be at least 62 years old and have paid into the system for at least 10 years to qualify for the benefits.

Most workers are covered by Social Security and are automatically enrolled when they start working. You may not be automatically covered if you work for the government or certain nonprofit organizations.

Social Security benefits are based on your lifetime earnings and provide protection for you and your family in the event of retirement, disability, or death.

When it comes to Social Security benefits, almost half or up to 85% of your benefits may be taxable if your income is above a certain amount. This is called provisional income. If your total income is below this base amount, then your Social Security benefits may not be taxed at all.

Here’s how you can figure out if your Social Security benefit is taxable:

For Single Filers:

- If you have a combined income of $25,000 to $34,000, you’ll have to pay taxes on up to 50% of your benefits.

- If your combined income is more than $34,000, you’ll have to pay taxes on up to 85% of your Social Security benefits.

For Married Couples Filing Jointly:

- If your combined income is between $32,000 and $44,000, you will pay taxes on up to 50% of your Social Security income.

- If your combined income is more than $44,000, you may have to pay taxes on up to 85% of your Social Security benefits.

If you have Social Security income that is taxable, the amount of taxes you pay will be based on your total combined retirement income. However, you’ll never pay taxes on more than 85% of your Social Security.

According to the Social Security Administration, you won’t have to pay taxes on your Social Security benefits if you file as an individual with a total income under $25,000. Also, If you’re married and file a joint return, you probably won’t pay any taxes on your Social Security benefits unless your combined income is more than $32,000.

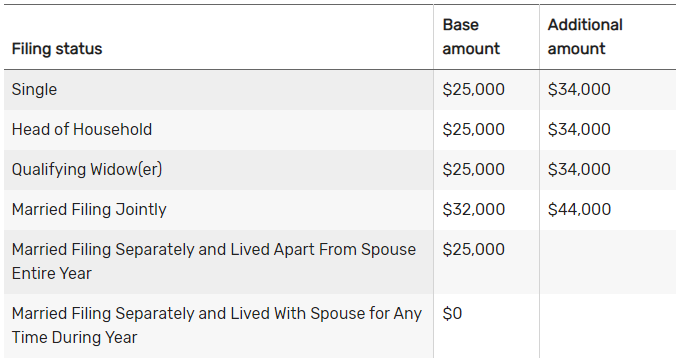

Calculating Taxes On Social Security Benefits

To calculate your tax liability, you must first determine your combined income. Your “combined income” is your adjusted gross income plus any nontaxable interest you have plus half of your social security benefits.

After you’ve calculated your combined income, use the table below to determine the amount of your benefits that will be taxable at your ordinary income tax rate.

Based on these base amounts, you can determine how much of your Social Security benefits are taxable.

In the case where a person’s income exceeds the base amount but not the additional amount, then 50% of their Social Security income is taxable. But when a person’s income exceeds the additional amount, then 85% of their Social Security income is taxable.

For example, let’s say if you’re a single filer and receive monthly benefits of $1,543, your annual benefits would be $18,516. Half of that is $9,258. Now let’s imagine you have a combined income of $30,000.

Then the taxable amount you’d enter on your federal income tax form is $5,000 (the difference between your combined income and your base amount of $25,000). This is because the taxable amount is lower than half of your annual Social Security benefit.

This is an example of someone paying taxes on 50% of their Social Security benefits. If you pay taxes on 85% of your benefits, things get complicated. However, the IRS offers software and a worksheet to help you calculate your Social Security tax liability.

How To File Social Security Benefits On Your Federal Taxes

You will need to file a Social Security income tax return if you received benefits from Social Security during the year and your total combined income (from all sources) is above a certain limit.

Each January, you will receive a Social Security Form SSA-1099. This form will show the total benefits you received in the previous year and how much you need to report to the IRS on your federal tax return.

If you misplaced your form, you can get a copy of your lost form whenever you want by creating a free account at the Social Security Administration.

Take the total amount shown in Box 5 of Form SSA-1099 and report it on line 6a of Form 1040 (your federal tax return) or Form 1040-SR (an alternative tax return for Seniors – age 65 or older).

State Taxes on Social Security

We’ve discussed everything above related to the federal income taxes. You may also have to pay state income taxes based on where you live.

Most states like California do not tax Social Security income, while some do.

Currently, there are 12 states that tax some or all of the benefits you receive. The following is a list of the states that tax Social Security income:

- Colorado

- Connecticut

- Kansas

- Minnesota

- Missouri

- Montana

- Nebraska

- New Mexico

- Rhode Island

- Utah

- Vermont

- West Virginia

All of these 12 states tax at least some Social Security benefits. Minnesota and Utah are two of those states that follow the same tax rules as the federal government.

Thus, if you live in one of those two states, you’ll have to pay the regular income tax rates for that state on all your taxable benefits (up to 85%).

There are also other states that follow the federal laws but offer deductions or exemptions based on your income or age. So, you will probably not pay tax on the full taxable amount in those nine states.

Social Security income is not taxable in the remaining 38 states (plus Washington, D.C.).

Conclusion

So, is Social Security taxable? The answer is usually yes. Up to 50% or 85% of your benefits may be taxable depending on how much other income you have in addition to your Social Security benefits.

The best way to determine how much tax you’ll owe on your Social Security benefits is to use the IRS worksheet or software. This will give you an accurate estimate of your tax liability.

However, most people who receive Social Security pay little to no taxes on their benefits because their incomes are low.

If you’re not sure whether or not your benefits are taxable, Consult with a tax professional.